How Your Investors Make Money: Venture Capital Fund Economics, Angel Returns, and What It Means for Your Raise

Understanding how venture funds, angel investors, and family offices make money changes how you negotiate. Here's the math behind their decisions.

How Your Investors Make Money: Venture Capital Fund Economics, Angel Returns, and What It Means for Your Raise

Why This Matters to You

Every investor sitting across the table from you is running their own business. A venture capital partner has fund economics, LP expectations, and a portfolio strategy that shapes every decision they make. An angel investor has personal financial constraints, a risk tolerance, and a target return that determines whether your deal is worth their time.

If you don’t understand how your investors make money, you can’t understand why they pass on deals, why they push for aggressive growth, why they block moderate exits, or why they stop funding underperformers. Knowing the math on the other side of the table makes you a better negotiator, a better board manager, and a more realistic fundraiser.

How a Venture Capital Fund Works

A venture fund is a pool of capital raised from limited partners (LPs), typically pension funds, endowments, fund-of-funds, and wealthy individuals. The fund has a fixed life (usually 10 years), a defined investment period (first 3-5 years), and a management structure.

The 2 and 20 model. Most venture funds charge a 2% annual management fee on committed capital and take 20% of profits (called carried interest or “carry”).

On a $100M fund:

- Management fees: $2M/year x 10 years = $20M over the life of the fund

- Investable capital after fees: ~$80M

- Carry: 20% of profits above the return of capital to LPs

The management fee pays salaries, rent, travel, and operations. On a $100M fund with a team of 4-5 people, $2M/year is a proper business. On a $10M fund, $200K/year barely covers one person’s salary. Most emerging managers can’t sustain a small fund indefinitely and either scale up or leave the business.

What LPs expect. A venture fund needs to return 3x net (after fees and carry) to be considered top quartile. Carta’s data on 2,904 US venture funds shows that median net TVPI (total value to paid-in capital) for 2017-2019 vintage funds sits around 1.2-1.5x, meaning the median fund barely returns capital after fees. Top quartile funds from those vintages show 1.7-2.5x net TVPI. Cambridge Associates data confirms that US VC returned 6.4% in H1 2025, barely outpacing public markets.

The spread between top and bottom quartile is enormous. A top-decile fund might return 5-10x, while a bottom-quartile fund returns less than 1x. There is no other asset class with this level of dispersion. LPs are betting on manager selection, not the asset class as a whole.

The Power Law

Venture returns follow a power-law distribution, not a normal distribution. A small number of investments generate the vast majority of returns. Everything else either fails or provides modest returns.

The distribution of outcomes across a fund’s portfolio looks roughly like this:

- 30-40% are total losses (investors lose everything)

- 20-30% break-even or return modest amounts

- 20-30% return 1-3x

- 10-15% return 3-10x

- Less than 5% return 10x or more

That last category makes the fund work.

This is the Airbnb example. Sequoia Capital invested nearly $600,000 in Airbnb’s 2009 seed round at $0.01 per share, acquiring about 58 million shares and roughly 70% of the total shares they would eventually own. That single check, written months after the financial crisis while Sequoia was sending portfolio companies a presentation titled “RIP Good Times,” was worth approximately $4.8 billion at IPO.

Over the following decade, Sequoia invested $260 million across the seed, Series A, D, and F rounds. The blended return they achieved was 1,746%. But the seed alone generated the vast majority of the value. The Information reported the full investor map at IPO: Y Combinator turned a $20,000 seed investment into $116 million. Youniversity Ventures (now Y Ventures, led by Keith Rabois and Kevin Hartz) turned $5 million into $302 million. Greylock’s Series A investment became worth $1.4 billion. Founders Fund’s $200 million across multiple rounds became $1.5 billion.

The Airbnb story also shows what happens when investors miss or misjudge. Andreessen Horowitz passed on the seed round, then invested $60 million at the Series A at a $1 billion valuation. They now own roughly 3% of the company. August Capital passed entirely and, according to their general partner, “deeply regrets” it.

Airbnb was an exception, not a median, and it’s worth understanding the conditions that produced that outcome. Sequoia invested its seed money at the lowest point of the 2008-2009 financial crisis. Airbnb benefited from the rising tide of the economic recovery, a shift in consumer behavior driven by the need for savings (people renting out spare rooms), the rise of the sharing economy, a decade of zero interest rate policy that fueled growth investing, a truly disruptive product with strong network effects, exceptional leadership, and investors who actively helped the company navigate rough patches. There were difficult moments along the way: the relationship between Sequoia and Chesky was rocky at times, fundraising for the Series C was harder than expected, and Airbnb still lacked veteran executive talent years into the business.

Above-average venture returns come from good pricing at entry, rising markets, a great product, great leadership, and a bit of luck. VCs get to roll the dice 10-20 times per fund. As a founder, you only have one opportunity to do that every 5-10 years. VCs want to invest in exceptions, not medians. The fund model depends on finding one Airbnb for every 20-30 investments that go to zero.

What this means for founders. When a VC passes on your deal, they’re usually not saying your company is bad. They’re saying it doesn’t look like a potential fund-returner given their portfolio math. A company that could grow to $50M in revenue is an excellent business, but if a fund needs $1B+ outcomes, a $50M revenue company won’t achieve meaningful results.

Why VCs Pass on Great Businesses

I get this question often from founders of fast-growing companies: “We’re profitable, growing quickly, and less risky than most startups. Why won’t VCs invest?”

Here’s a concrete example. Consider a company doing $1M in revenue, growing at 50% year over year. Over six years, revenue compounds to $11.4M. The company sells for 3.9x revenue (a confirmed market multiple for acquisitions in this range), producing a $44.4M exit. Sustained 50% annual growth for six years is remarkable for any business outside of venture-backed software. This is a top-tier outcome by almost any measure.

Assume the company raised a $1.5M seed round from three investors at a $10M post-money valuation, with a 10% option pool.

| Stakeholder | Ownership | Payout at $44.4M Exit |

|---|---|---|

| Founders (combined) | 75% | $33.3M |

| Employees (option pool) | 10% | $4.4M |

| Investor A | 5% | $2.2M |

| Investor B | 5% | $2.2M |

| Investor C | 5% | $2.2M |

Each investor gets $2.2M back on a $500K check. That’s a 4.4x return over 7 years, roughly 24% annualized. Better than almost any other asset class. The founders take home $33.3M. The employees split $4.4M. Everyone made money.

Now put that deal inside a $50M venture fund. The fund owns 5% and receives $2.2M, which is 4.4% of the fund. If every company in the 30-company portfolio produced this exact outcome (which would be miraculous), the fund would return 30 x $2.2M = $66M gross. After carry, LPs get about $63M on their $50M commitment. That’s a 1.26x net return, which is below the median venture fund.

A $44.4M exit on 50% annual growth over six years generates life-changing wealth for the founders, strong returns for individual investors, and is statistically irrelevant to a venture fund. The business isn’t the problem. The structural mismatch between what good businesses produce and what venture fund economics require is the problem. VCs aren’t choosing bad companies over good ones. They’re choosing a small chance at a $500M outcome over a high probability of a $44M outcome, because that is the only math that returns their fund.

The right investors for this company are angels who treat $500K as a meaningful personal bet, family offices that value steady growth over exponential scale, or strategic acquirers in the industry who see the revenue and the customer base as assets worth paying for. Matching the investor to the business means understanding what “success” looks like on both sides of the table.

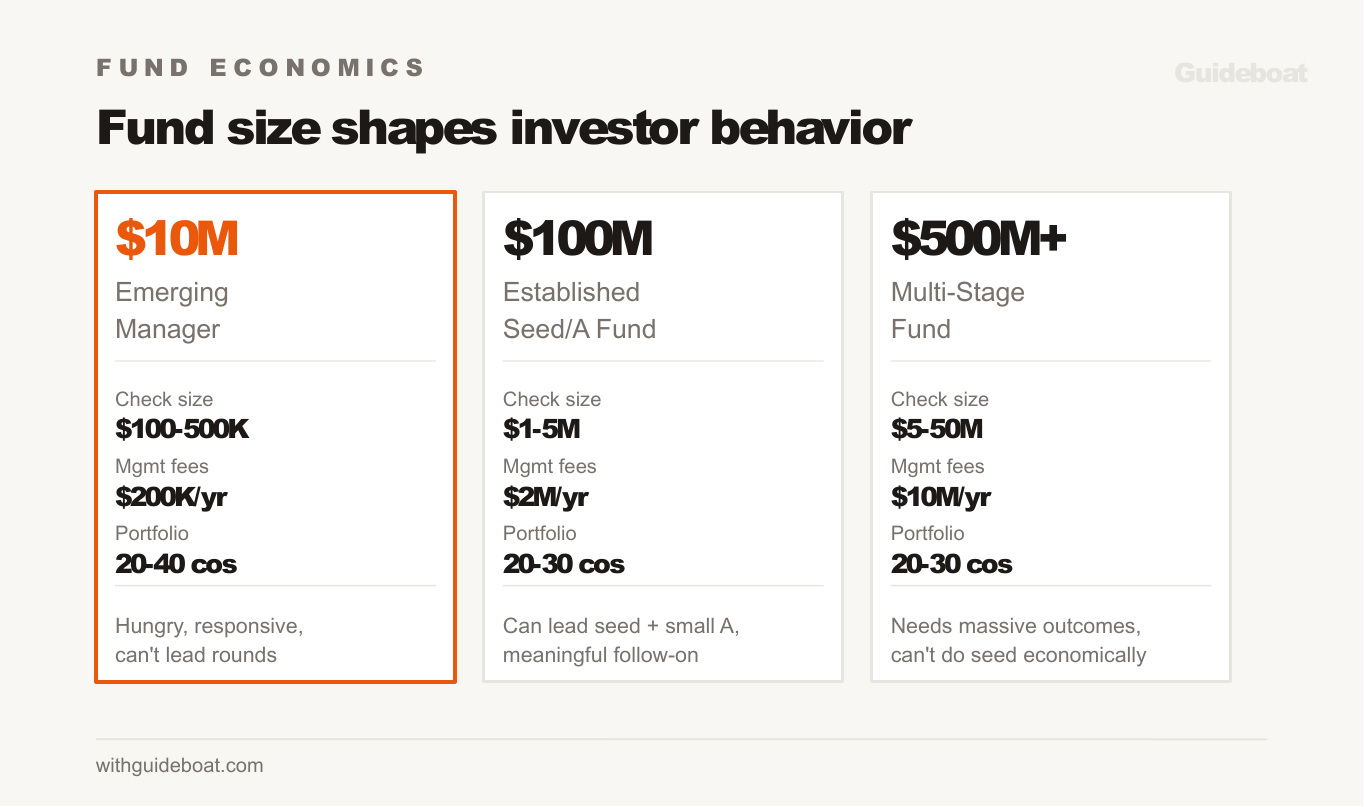

Fund Size Shapes Behavior

The size of a fund determines how its managers invest, what they look for, and how they treat you.

A $10M fund (emerging manager). After management fees, roughly $8M is investable. Initial check sizes of $100-250K with limited follow-on reserves mean the manager is building a portfolio of 30-50+ companies. Management fees are $200K/year, which means the GP is paying themselves below market salary and betting on carry. These managers are hungry, responsive, and often more founder-friendly because they need winners badly. But the fund can’t lead rounds, follow-on capital is limited, and every deal needs co-investors.

A $100M fund (established seed/Series A). After fees, roughly $80M is investable. Most seed funds reserve 40-60% of the fund for follow-on investments in their best-performing companies, leaving $30-50M for initial checks. At $500K-$1M per initial check, that’s 30-60+ portfolio companies. Management fees support a team of 4-6. These funds can lead seed rounds and participate in Series A deals. Their LPs expect 3x net returns, which means the fund needs to return $300M on $80M of investable capital.

A $500M+ fund (multi-stage). Check sizes of $5-50M. These funds need massive outcomes. A $500K seed check is economically irrelevant to them because even a 100x return ($50M) doesn’t matter at fund scale. Therefore, large funds write large checks, which means they need later-stage companies or companies raising big rounds. When you hear “we don’t do seed,” it’s not a preference. It’s math.

The path from Fund I to Fund III. An emerging manager raising a first fund of $10-25M needs to show returns to attract LPs for Fund II. The problem: most seed investments haven’t matured enough to show realized returns (DPI, distributions to paid-in capital) by the time the manager needs to fundraise again (usually 2-3 years into Fund I). So Fund II often gets raised on paper markups (TVPI) and qualitative signals (which portfolio companies raised follow-on rounds, who graduated from seed to Series A).

Carta’s data shows that seed-to-Series A graduation rates have declined, with no post-Q3-2021 cohort exceeding 30%. For an emerging manager with 20 seed investments, that means 6 might raise a Series A, which is the primary markup event that makes the portfolio look good for Fund II fundraising. If fewer graduate, the manager struggles to raise the next fund regardless of their judgment or effort.

Angel Investor Economics

Angel investors operate under completely different constraints. They’re investing personal capital, not fund capital. There are no management fees, no carry structure, and no LP expectations. But the math is still unforgiving.

Who are angel investors? The SEC requires accredited investor status: $200K+ individual income ($300K joint) or $1M+ net worth excluding primary residence. As we’ve written about previously, those thresholds haven’t changed since 1982. Adjusted for inflation, they’d be roughly $600K income and $2.8M net worth today. The bar has eroded, but most angels are still people with meaningful but not unlimited capital.

The typical angel. Consider someone earning $300K/year in a high-cost metro. After taxes, housing, childcare, retirement contributions, and living expenses, disposable capital for angel investing might be $50-100K/year. At $25K per check, that’s 2-4 deals per year. Over a 5-year investing period, that’s a portfolio of 10-20 companies.

Portfolio return math. Apply the same power law that governs venture funds:

- 50% of investments go to zero (more aggressive than VC because angels invest earlier)

- 30% return 0-1x

- 15% return 1-3x

- 5% return 3x+

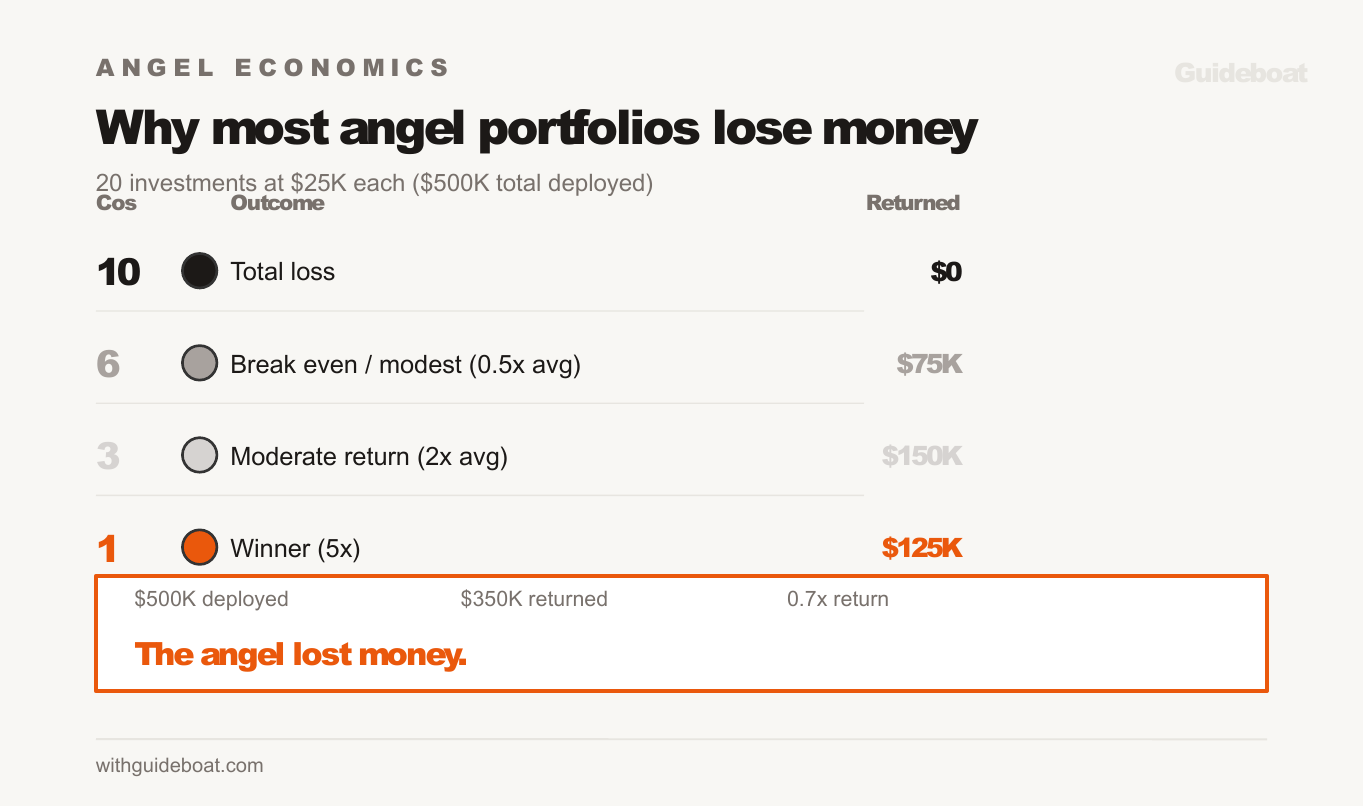

On a portfolio of 20 investments at $25K each ($500K total deployed):

- 10 companies return $0

- 6 companies return an average of $12.5K each = $75K

- 3 companies return an average of $50K each = $150K

- 1 company returns 5x = $125K

Total returned: $350K on $500K invested. That’s a 0.7x return. The angel lost money.

To break even, the portfolio needs one investment that returns 10x+ or several that return 3-5x. To beat the S&P 500 (roughly 10% annualized over 7 years = 2x), the portfolio needs a standout performer returning 20x+ or a cluster of 5-10x returns.

This is why most angels lose money. The math only works with sufficient deal flow, strong selection, and enough portfolio size to capture a power law outcome. An angel doing 2 deals per year doesn’t have enough shots on goal. An angel writing $10K checks doesn’t have enough ownership to matter even when a company succeeds.

The high-net-worth angel is a different animal. An individual with $10M+ in investable assets has access to a different set of options. With $100-500K checks, they can purchase significant ownership. A pace of 10-15 deals per year gives the portfolio enough breadth to capture power law returns. Pre-IPO allocations, SPVs, and fund commitments become available at this level that smaller angels can’t access. At this point, angel investing starts to look more like running a micro-fund with personal capital.

Why some angels beat the math. Private company investing is one of the only places where an investor can do something to change the enterprise value of the company. An investor can buy shares of Apple, but nothing they do as an individual will change what Apple is worth. An angel investor can put $50K into a startup and then introduce the founder to a distribution partner that triples revenue, connect them with a compliance expert who saves six months of regulatory work, or help them recruit a CTO who transforms the product.

This is the concept of investor-startup fit, and it matters as much as founder-market fit. Angels who generate above-average returns don’t sit passively on their investments. They plant a flag and work alongside founders to create enterprise value. That’s an extraordinary opportunity, and it’s one reason people angel invest despite the brutal math. The financial return expectation may be negative, but the ability to influence the outcome directly makes it a fundamentally different asset class than public equities.

There is a lot of talk in the venture world about “value add,” but it becomes much harder for VCs to deliver at scale when they’re managing 20-30 portfolio companies. It is worth asking a potential investor exactly how they have added value to their portfolio companies, and pushing for that value to materialize after they invest. You should align the value they add with specific gaps in your organization: distribution, product, leadership, compliance, strategy, whatever the business actually needs.

What founders should know about their angels. The angel writing a $25K check is probably investing a meaningful percentage of their disposable capital. They care about the outcome, but they likely don’t have the portfolio construction to expect venture-scale returns. Be honest with them about the risks. The angel writing a $250K check is operating closer to an institutional investor and will have correspondingly higher expectations for governance, information rights, and return potential.

What the Market Data Shows

The venture capital market in 2025-2026 reflects several structural realities that affect founders:

Capital is concentrated. The top 12 VC firms captured over 50% of all capital raised in H1 2025. The top 1% of deals received 33% of all capital deployed. AI companies absorbed 65.4% of the total deal value in 2025. If you’re not in AI and you’re not raising from a top-tier fund, you’re competing for a shrinking pool of capital.

Fundraising is at a seven-year low. New fund formation declined 20% year-over-year. This means fewer new funds entering the market, which means fewer investors making first-time bets on new companies. Established funds are doing more follow-on into existing portfolio companies rather than making new investments.

Graduation rates are declining. Carta’s data shows that seed-to-Series A graduation rates have fallen, with no cohort since Q3 2021 exceeding 30%. PitchBook data shows only 3% of seed companies raise a Series A within 12 months. The funnel is getting narrower.

Returns are compressing. Cambridge Associates reports US VC returned 6.4% in H1 2025. The rolling one-year IRR for venture sits at 7.8%. VC has called 1.6x more capital than it has distributed since 2022. LPs are getting impatient with paper markups and demanding cash returns. This pressure flows downhill to founders as tighter terms, lower valuations, and more scrutiny on burn rate and path to profitability.

Return Expectations by Investor Type

When you’re negotiating with investors, their return expectations shape everything:

| Investor Type | Typical Check | Target Return | Time Horizon | What They Need From You |

|---|---|---|---|---|

| Angel ($1-3M NW) | $10-50K | 3-5x (hope for 10x) | 5-10 years | Equity upside, a good story, trust |

| Angel ($10M+ NW) | $100-500K | 5-10x | 5-7 years | Ownership, governance, information |

| Angel group / syndicate | $50-250K pooled | 3-5x net | 5-10 years | Structured process, clear terms |

| Seed fund ($10-50M) | $250K-$2M | 10-30x on winners | 7-10 years | Fund-returner potential |

| Series A fund ($100-500M) | $5-25M | 10-20x on winners | 7-10 years | Market leadership path |

| Family office | $100K-$5M | 2-5x (varies widely) | Flexible | Relationship, trust, co-investment |

| Strategic / corporate | $250K-$10M | Strategic value first | Varies | Market access, technology, data |

The key insight is that the smaller the check, the more personal the relationship, and the more flexible the return expectation. A larger check signifies a more institutional process with a more rigid return requirement.

What This Means for Your Fundraise

Match the investor to the business. A $5M revenue company growing 30% annually is a great business, but a terrible venture investment. Raising from a VC fund that needs 10x returns will create a governance nightmare. Raising from angels or a family office that expects 3-5x creates alignment.

Understand why they pass. When a VC says “This isn’t a fit for our fund,” they’re usually being literal. Your company doesn’t fit their portfolio math. It’s not a judgment on the business.

Know what happens when the fund’s incentives diverge from yours. A board member who represents a fund will eventually have to choose between what’s best for the company and what’s best for the fund. In most cases, the company and the fund share the same interests. When they diverge (you want to sell for $30M, the fund needs a $300M outcome), the fund’s interests win because they have contractual rights that you agreed to in the term sheet.

Negotiate from understanding, not from ignorance. When you know that a $100M fund needs 3x net returns and has invested $3M in your company, you can calculate what they need your company to be worth for the math to work. That knowledge changes how you negotiate valuation, how you set milestones, and how you communicate progress.

The Bottom Line

Your investors are not your friends, your enemies, or your bosses. They are business partners with their own economics. Mutual understanding of those economics builds the best founder-investor relationships: it covers what each side needs, what each side risks, and what success looks like for both.

Before you take anyone’s money, understand how they make theirs.

Further Reading

- NVCA 2025 Yearbook - venture capital industry data

- AngelList Fund Benchmarks Report 2025 - emerging manager fund performance

- Carta Data - IRR, TVPI, and DPI by vintage and quartile

- Cambridge Associates: US VC Benchmark - long-term VC returns vs. public markets

- Harvard Business School: The Venture Capital Secret - why 75% of VC-backed companies never return cash

Understanding your investor’s business model is the foundation of a productive fundraising relationship. Should You Raise Venture Capital? helps you decide whether VC is right for your company. SAFE vs. Convertible Note vs. Priced Round covers the instruments, and What Is a Cap Table? explains how ownership evolves as you raise.