Accredited Investors: What Founders Need to Know

What an accredited investor is, why it matters for your fundraise, and what paperwork to collect. A founder's guide to the SEC requirements and how to stay compliant.

Accredited Investors: What Founders Need to Know

A note before we start: This is not legal advice. Securities law is complex, state-specific, and the penalties for getting it wrong are serious. This article reflects my experience working with startups and investors over the last 10 years. Use it as a starting point for conversations with your attorney, not as a substitute.

The Short Version

An accredited investor is someone the SEC says can invest in private securities: startup equity, fund interests, private placements. The qualification is based on income, net worth, or professional credentials. Most startup fundraising under Regulation D requires your investors to meet this bar. Reg D is the rule that governs most startup investments and states the rules of the road in terms of how you as a founder can accept investor dollars.

From a founder’s perspective, the accredited investor standard determines your investor pool, your compliance obligations, and the paperwork you need to collect before taking anyone’s money. Get it wrong and you have a securities violation that will surface during your next round’s legal diligence, when it’s most expensive to fix.

Who Qualifies?

You qualify as an accredited investor if you meet any of these criteria:

Income test. Individuals earned over $200,000 in each of the last two years, and they expect earning the same income this year. With a spouse or domestic partner, a joint income exceeding $300,000 also meets these conditions.

Net worth test. A net worth that exceeds $1,000,000, not including your primary residence. This includes bank accounts, brokerage accounts, retirement funds, and real estate other than your home, minus all debts.

Professional certifications. License holders of Series 7, Series 65, or Series 82 who are in good standing. Added in 2020 to recognize financial expertise beyond personal wealth.

Insiders and fund employees. Executive officers, directors, or general partners of the issuing company or fund are qualified. So do employees of private funds who take part in investment decisions.

Entity test. Entities with over $5M in assets qualify: trusts, LLCs, corporations, partnerships. Banks, insurance companies, and registered investment companies also qualify regardless of size. This matters when you’re taking investment from a family office, an angel group’s SPV, or a corporate venture arm. The entity itself needs to meet the threshold, not the individuals behind it.

One important note: the dollar thresholds ($200K/$300K income, $1M net worth) have not changed since 1982. Adjusted for inflation, those numbers would be roughly $600K and $2.8 million today. Congress has discussed updating them but hasn’t acted. The practical effect is that the pool of accredited investors has grown substantially over four decades, not because the standard has loosened, but because inflation has eroded the bar.

Why Founders Should Care

The accredited investor standard is not an abstract regulatory concept. It directly controls how you raise money:

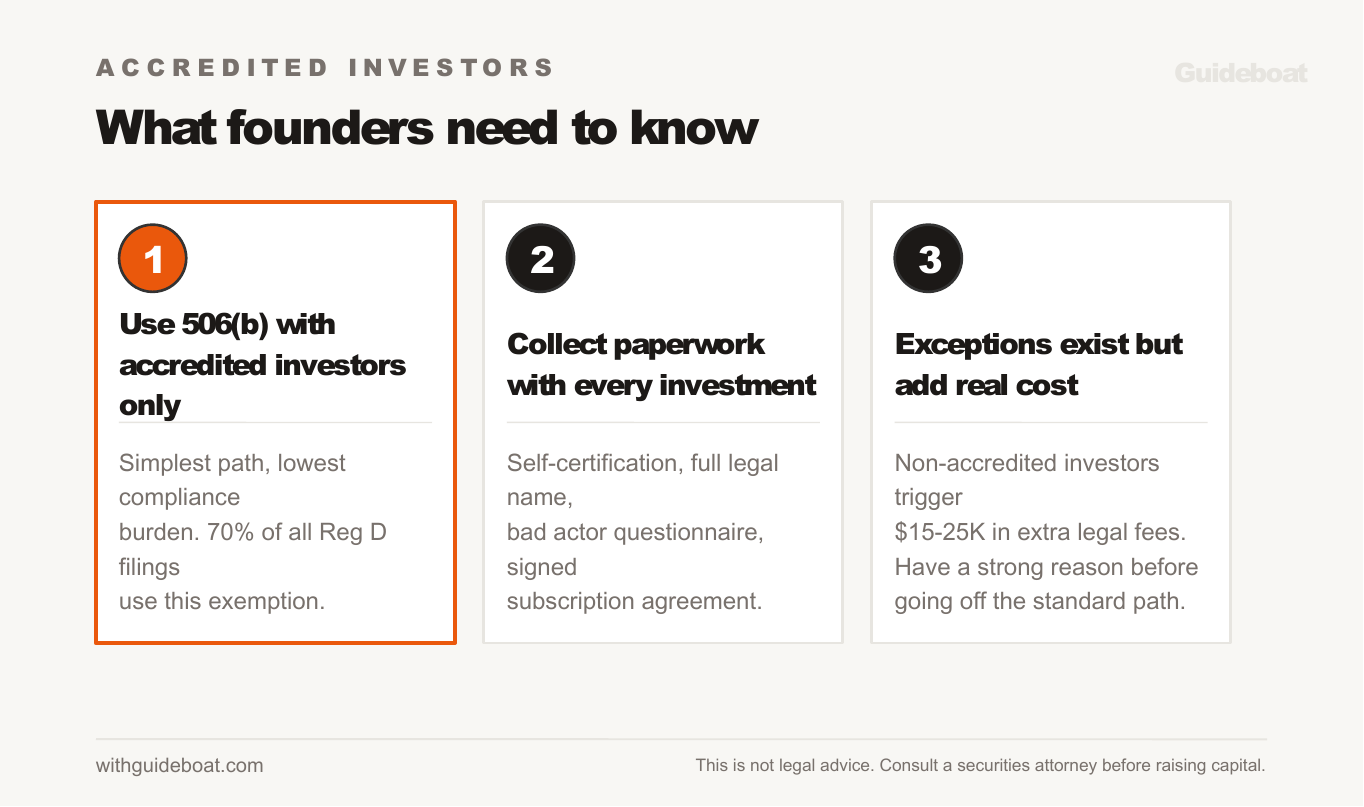

Under Reg D 506(b), the most common exemption for startup fundraising, you can raise unlimited capital from accredited investors without registering with the SEC. You can include up to 35 non-accredited investors, but doing so triggers heavy disclosure requirements (essentially a mini-prospectus) and prohibits public marketing of the raise. The compliance cost for including non-accredited investors in a 506(b) round typically runs $15-25K in additional legal fees. For most seed rounds, that cost is not worth a few small checks.

Under Reg D 506(c), you can publicly announce your raise, post on LinkedIn, and do press about it. However, you must ensure every investor is accredited and verify their status using a third-party method. Self-certification is not sufficient. From what I’ve seen working with companies, 506(c) was not faster than 506(b) and did not bring in additional investors. For companies that are difficult for most consumers to understand (deep tech, B2B software, industrial products), public marketing of the round did not unlock a new pool of investors that wasn’t already available through warm introductions and targeted outreach. It added friction to the process without a corresponding benefit.

Under Reg CF, there is no accreditation requirement. Anyone can invest. But you’re limited to $5M per year and must use a registered crowdfunding platform. Sara Hanks, CEO of CrowdCheck and former SEC Division of Corporation Finance attorney, has spent over a decade working on Reg CF compliance. If you’re considering this path, CrowdCheck provides due diligence and disclosure services specifically for crowdfunding offerings. But for most startups, Reg CF is a narrow tool: the median raise is $114K, the platforms take a cut, and the investor base skews toward retail participants who are less likely to provide the strategic value that early-stage companies need.

Under Reg A+, there is also no accreditation requirement. You can raise up to $75M. But the SEC qualification process takes 3-6 months, costs $150-500K+, and requires audited financial statements both for the offering and on an ongoing annual basis. This is a path for companies with significant resources, an existing finance team, and a specific reason to access retail investors.

My recommendation for most founders raising an angel or seed round: use 506(b) with accredited investors only. It is the simplest path with the lowest compliance burden. You can include non-accredited investors or raise under different exemptions, but the additional regulatory requirements, legal costs, and compliance risks are substantial. Unless you have a compelling strategic reason to make an exception (for example, a key industry partner who doesn’t meet the thresholds but brings critical value to the business), keep your round accredited-only and save yourself the headache.

What to Do When You Take an Investment

This is the operational part that most articles skip. When an investor commits capital, you need to collect specific information and paperwork. Consider this a checklist for your signing packet.

1. Accredited investor self-certification. Under 506(b), the investor signs a form representing that they meet one of the SEC criteria. This is typically part of the subscription agreement. Keep the signed form in your data room. If you’re raising under 506(c), self-certification is not enough, and you’ll need third-party verification (see below). Your lawyer can provide you with a self-attestation template for the signing packet.

2. Full legal name and entity information. Get the investor’s full legal name as it should appear on the cap table and all legal documents. If the investment is coming from an entity (an LLC, trust, or fund), get the full entity name, the state of formation, and the name of the authorized signatory. Cap table errors from incorrect names are surprisingly common and create headaches during future diligence.

3. Bad actor questionnaire. SEC Rule 506(d) disqualifies “bad actors” from participating in Reg D offerings. This covers individuals with certain criminal convictions, SEC enforcement actions, or other regulatory disqualifications. Include a bad actor self-certification in your subscription documents where the investor represents they are not a bad actor under Rule 506(d). Failing to screen for a bad actor who invests in your round can invalidate the entire exemption. This is a low-probability event with catastrophic consequences if it happens, so screen for it every time.

4. Signed subscription agreement. This is the actual investment contract. It should include the self-certification, the bad actor representation, the investment amount, the terms of the instrument (SAFE, convertible note, or equity), and the date.

5. Wire confirmation or proof of payment. Confirm receipt of funds and keep records.

This paperwork takes 15 minutes per investor and protects you for years. Skipping it feels harmless in the moment but creates real liability. Joe Wallin, a startup securities attorney who writes the Startup Law Blog, has documented extensively how small compliance oversights in early rounds compound into serious problems during later fundraising. His advice to founders is consistent: get the paperwork right from the beginning, because cleaning it up later costs 10x more.

Verification Methods (for 506(c) Raises)

If you’re raising under 506(c) and want the ability to publicly market your round, self-certification isn’t enough. The SEC requires “reasonable steps” to verify each investor. Four safe-harbor methods qualify:

- Income verification: Review tax returns or W-2s for the last two years, plus a written representation about expected income this year.

- Net worth verification: Review bank statements, brokerage statements, and a credit report. Assets minus debts must exceed $1M (excluding primary residence).

- Third-party letter: A licensed broker-dealer, investment adviser, attorney, or CPA confirms the investor’s status in writing.

- Prior verification: If the verification of the investor occurred within the last three months, you can rely on that verification along with a written confirmation that their status hasn’t changed.

Third-party services like VerifyInvestor handle this for you. They collect documents, confirm status, and issue verification letters. Costs run $30-100 per investor.

Most seed-stage founders use 506(b) and avoid this entirely. Switch to 506(c) only if public marketing is strategically important for your round.

Accredited Investor vs. Qualified Purchaser

A related but distinct concept: a qualified purchaser is a higher bar. Individuals must own $5M or more in investments (not net worth, specifically investments). Entities need $25M.

This matters if you encounter it in fund structures. Funds with over 100 investors need all participants to be qualified purchasers (not merely accredited) to avoid full Investment Company Act registration. For direct startup investment, the accredited investor standard applies. You’ll encounter the qualified purchaser distinction primarily with hedge funds, PE funds, and venture fund LPs.

The 2020 Rule Changes

In August 2020, the SEC expanded the accredited investor definition for the first time since 1982:

- Professional certifications added. Series 7, 65, and 82 holders now qualify regardless of income or net worth.

- Spousal pooling expanded. Unmarried domestic partners can now combine finances for the income and net worth tests.

- Fund employees included. Private fund employees who participate in investment decisions qualify, even without meeting income or net worth tests.

- Entity definition broadened. LLCs, registered investment advisers, and family offices with over $5 million in assets now qualify.

The SEC has signaled interest in further changes, potentially adjusting the income and net worth thresholds or adding additional qualification paths. Any changes will take time to implement, but founders should know the definition may evolve.

The Market Data: Where Founders Actually Raise

The numbers confirm what experience suggests. The vast majority of private capital flows through Reg D, and most of that is 506(b).

- Reg D accounted for $2.4 trillion in capital raised in 2025. Approximately 70% of new filings used 506(b), with 30% electing 506(c). That 30% is heavily weighted toward real estate syndications and fund offerings, not startup rounds.

- Reg CF raised $378 million in 2025, with a median raise of $114K and an average of $368K. That is a fraction of the Reg D market.

- Reg A+ is a small and declining segment of exempt offerings.

For startup founders, the takeaway is straightforward: Reg D 506(b) with accredited investors is the standard path because it is where the capital is; the compliance is manageable, and lawyers, investors, and founders all understand the process. The alternatives exist for specific situations, but they are not the default for a reason. My advice is to think seriously about the trade-offs before going off the well-trodden path.

The Bottom Line

For founders, the accredited investor standard is a compliance requirement that governs who can write you a check. Get the paperwork right from the beginning: collect self-certifications, full legal names, and bad actor questionnaires with every investment. Keep everything in your data room. These steps take minutes per investor and prevent problems that cost months and thousands of dollars to fix during future due diligence.

If you want non-accredited investors in your round, understand the trade-offs: Reg CF gives you access but limits the raise to $5M through a platform. Including non-accredited investors in a 506(b) round adds $15-25K in legal costs. For most early-stage raises, keeping it accredited-only is the right call.

Further Reading

- SEC: Accredited Investors - the official definition and recent updates

- SEC: Rule 506(d) Bad Actor Disqualification - what disqualifies an investor from Reg D participation

- Joe Wallin’s Startup Law Blog - practical securities law guidance for founders

- CrowdCheck - compliance and due diligence for Reg CF offerings

- VerifyInvestor - third-party accreditation verification service

- Y Combinator SAFE Documents - standard subscription documents that include accreditation representations

Our Regulation D Founder’s Guide offers more information on the regulatory framework’s impact on your fundraise. How to Raise Money for a Startup covers the full fundraising process, and What Goes in a Startup Data Room explains how to organize your investor documents.