What Goes in a Startup Data Room

A startup data room is the organized collection of documents investors review during due diligence. Here's what to include, how to organize it, and how to use it strategically.

What Goes in a Startup Data Room

The Short Version

A data room is a folder or shared drive where all the supporting documents an investor would need to invest in your company live. It is used as part of the investment diligence and closing process. But it also serves two functions that most fundraising guides don’t talk about.

First, having your business documents organized is operational discipline, not a fundraising artifact. You should have your corporate records, financials, contracts, and cap table organized for yourself. For governance, for strategy, for not wasting time on administrative search every time someone asks you a question about your own company. If you’re assembling these documents for investors, you’re already behind. The investor benefit is a side effect of running an organized business.

Second, diligence is a process of escalating commitment. Every document request is a touchpoint in a relationship, not a box to check. Each interaction where the investor invests their time (reviewing your financials, asking about a contract, scheduling a follow-up call) makes them more likely to move forward. The founders who understand this don’t dump everything into a folder on day one. They control the flow of information and use each document release as a reason to deepen the conversation.

Two principles drive everything that follows: luck favors the prepared, and negotiations are built on escalating commitment.

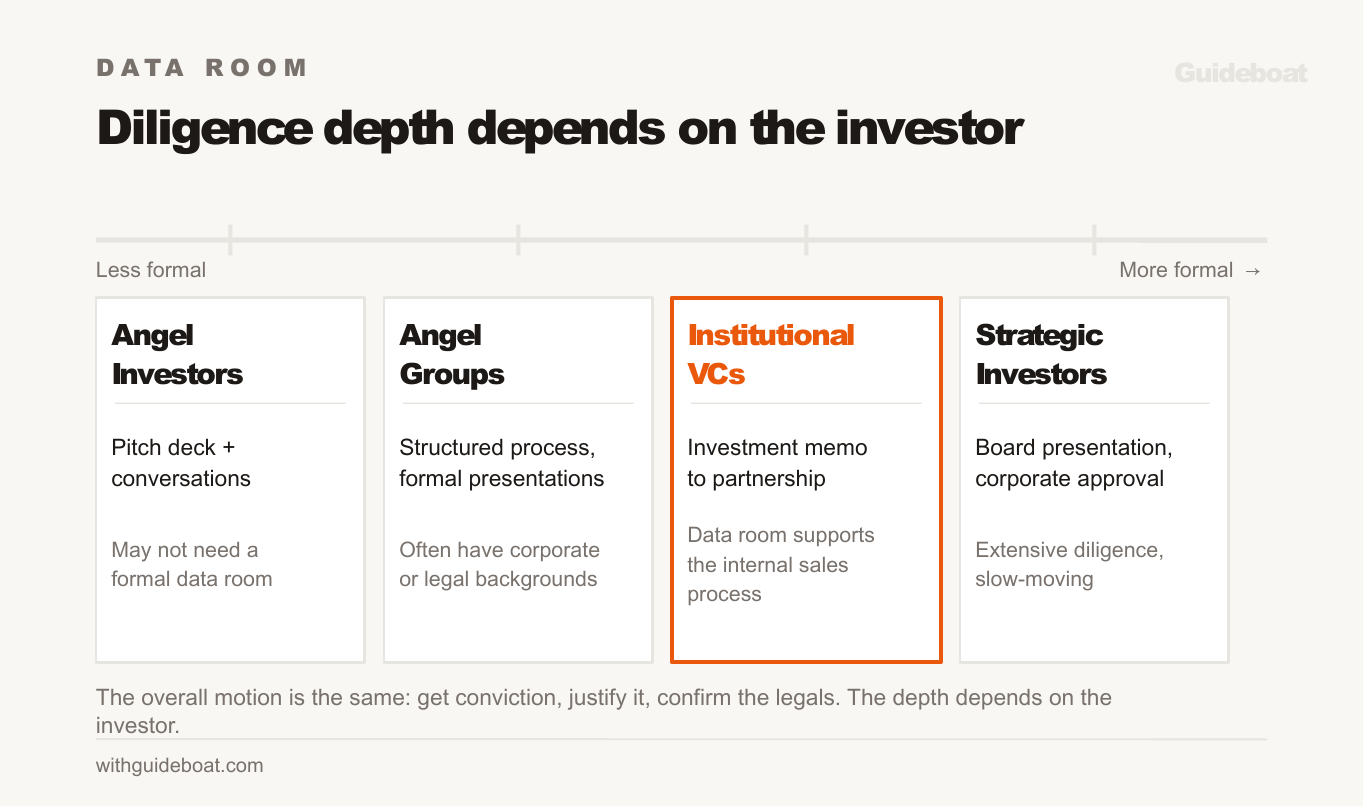

The Diligence Process Depends on the Investor

The structure of your data room and the depth of diligence changes depending on the investor type and the type of investment. This is the most important thing to understand before you start organizing documents.

Angel investors may not require a formal data room at all. Many early-stage angel deals get done on a pitch deck and a series of conversations. The investor gets conviction through direct interaction with the founder, and the investment documents arrive over DocuSign or from the startup’s lawyer. Preparing a 200-document data room for an angel writing a $50K check is overkill and could slow down a deal that would otherwise close on momentum and trust.

Institutional VCs work differently. Partners at larger funds need to draft an investment memo to justify the deal, then present and defend that memo to an internal committee or the firm’s partners. The diligence process is structured around building the case for that memo: validating the market, researching the competition, stress-testing the financials, and getting conviction on the team. Your data room documents are supporting material in a sales process. You are not selling to the partner across the table from you. You are selling to the investment committee that partner has to convince.

Angel groups and local investor networks often fall somewhere in between. These investors may have more experience in corporate finance or legal backgrounds, and their processes tend to be more formal because that is how they are accustomed to measuring and justifying risk. Expect more structured diligence from these groups than from individual angels.

Strategic investors (corporations investing for business reasons) have their own internal approval processes, which may involve presenting to a corporate board. The diligence there can be extensive and slow-moving, driven by corporate legal and finance teams rather than a single decision-maker.

The overall motion is the same regardless of investor type: get conviction about the business, justify that conviction, then confirm the legal details. But the depth and formality of each step depends on the experience and requirements of each investor. Your job during the process is to understand what the investor needs to make their decision, whether that is a personal conversation over coffee, a 40-page investment memo, or a board presentation, and position them for success.

What Goes in a Startup Data Room

With that framework in mind, here is the full document checklist organized by when investors typically ask for each item. I’ve reviewed data rooms for deals ranging from $100K to $10M or more.

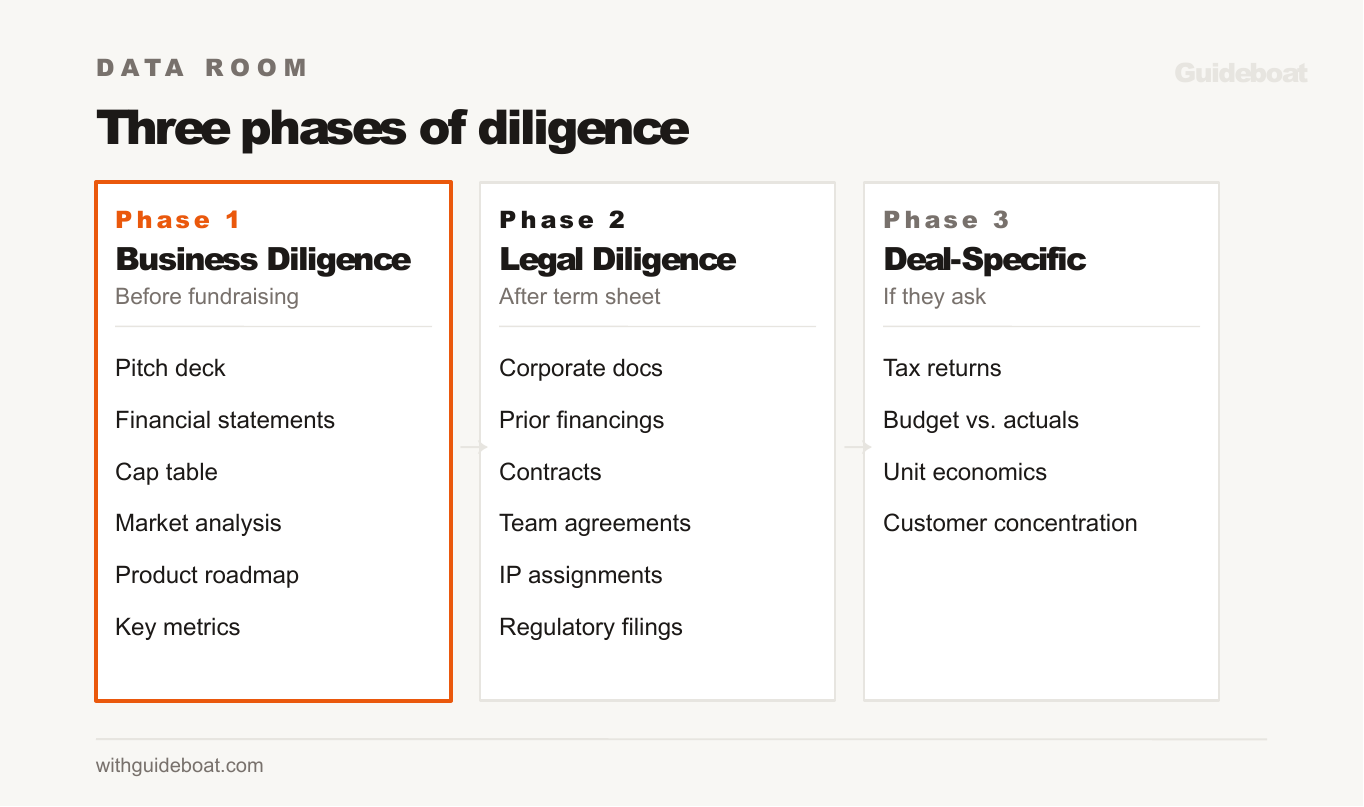

Phase 1: Business Diligence (Prove the Opportunity)

Phase 1 is about validating the claims in your pitch deck: the market opportunity, the competitive landscape, the team, and the financial trajectory. For institutional VCs, this is the material that goes into the investment memo. For angels and family offices, this is what builds enough conviction to move forward. Everything in Phase 1 should help the investor answer the question: is this a deal worth pursuing?

Pitch materials

- Current investor deck

- One-pager or executive summary

Financial statements

- Income statement, balance sheet, and cash flow statement if the company is older than 6 months

- Current bank statements to demonstrate existing runway

- Financial projections (the same model you’re presenting in your pitch)

Cap table

- Current cap table showing all shareholders, option holders, and outstanding convertible instruments (SAFEs, notes)

- Vesting schedules for all founders and employees

- 409A valuation (if you’ve issued options)

Market and competitive

- Market sizing analysis (the full workup, not the slide alone)

- Competitive landscape analysis

- Key metrics dashboard

Product

- Product roadmap

- Technical architecture overview (for technical investors)

- Customer testimonials or case studies

Phase 2: Legal Diligence (Confirm Nothing Is Broken)

Legal diligence is confirmation work: verifying that the corporate structure, ownership, and agreements are clean. For institutional VCs, this typically starts after the investor has conviction and a term sheet is on the table. For angels and family offices, it may happen earlier or in parallel with business diligence.

How the round is organized also matters. A priced equity round with a lead investor involves more legal coordination than a rolling close on SAFEs, because the lead may negotiate governance terms like board seats, information rights, or pro rata provisions that affect every other participant in the round. The politics of who is leading, who is following, and how investors communicate with each other during this phase can be as important as the documents themselves.

Corporate documents

- Certificate of incorporation and all amendments

- Bylaws or operating agreement

- Board consents and meeting minutes

- Good standing certificate

- State registrations (if operating in multiple states)

Prior financings

- Signed stock purchase agreements, option grants, and SAFE/note documents

Contracts and agreements

- Key customer contracts or LOIs

- Vendor and supplier agreements

- Partnership agreements

- Office lease

- Insurance agreements

Team

- Organizational chart

- Founder bios and LinkedIn profiles

- Employment agreements (especially any with unusual terms)

- Contractor agreements (especially for IP-related work)

- Employee option plan (the plan itself, not the grants alone)

Intellectual property

- Patent filings or issued patents

- Trademark registrations

- IP assignment agreements (critical: make sure all IP created by founders and contractors is assigned to the company, not the individual)

Legal

- Pending or threatened litigation

- Regulatory filings or approvals

- Material correspondence with regulators

Phase 3: Deal-Specific Requests

These depend on the investor, the round size, and the industry.

Tax

- Recent tax returns

- Outstanding tax issues

Additional financial detail

- Budget vs. actuals comparison

- Revenue cohort data or unit economics breakdown

- Customer concentration analysis

How to Build Your Data Room

You do not need a fancy platform. For pre-seed and seed rounds, Google Drive is sufficient. Here is exactly how to set it up.

Step 1: Create your master folder. Create a Google Drive folder called [Company Name] - Master Data Room. This is your internal reference. Put everything here: corporate docs, market research, product descriptions, evidence of traction (testimonials, cohort analysis, financials, whatever you have). Organize it by the Phase 1 / Phase 2 / Phase 3 categories above. This folder is for you, not for investors. Keep it current. If you want to be organized, add a Google Sheet to the folder as an index: every document listed with a link, a brief description, and the date it was last updated.

Step 2: Create a shareable decks folder. Create a separate folder called [Company Name] - Shareable Decks. Put your teaser deck and your full investor deck here. Set the link so “anyone with the link can view.” This resolves the sharing visibility issue because you’re sending a link, not inviting people to a shared folder. You’ll send this link to a lot of people. Don’t track who views it at this stage.

Step 3: Create individual investor folders when diligence starts. When an investor asks for more than the deck (a financial model, customer data, contracts), create a new folder called [Investor Name] - [Company Name] - Data Room. Copy only the files they’ve asked for from your master folder into this investor-specific folder. Share it with only that investor, set to view-only. This way each investor sees only what you’ve chosen to share with them, and no investor can see who else has access.

Step 4: Track what you’ve shared. In your master folder index (the Google Sheet), add a column for each investor you’re in active diligence with. Mark which documents you’ve shared with each one. This becomes your control panel for managing information flow across multiple conversations.

Step 5: Keep the master updated. If you update a file in the master folder, update it in every investor folder that contains that file. Investors should always be looking at your most current information.

When to upgrade from Google Drive. If managing individual folders becomes unwieldy (more than 5-6 investors in active diligence simultaneously), or if you want analytics on who’s viewing which documents and for how long, it’s time to pay for a platform. DocSend is the most common choice for seed and Series A raises. It’s part of Dropbox, well-respected, and intuitive. The data room feature runs $150-200/month, so expect to spend roughly $1,000 over the course of a fundraise. Ansarada is another solid option common in venture deals. For larger rounds (Series B+) or M&A transactions, dedicated platforms like Intralinks and Datasite offer full audit trails and page-level viewing analytics, but they’re overkill for anything below a $10M round.

Make them show up. A data room should give investors enough to stay engaged, not enough to make a decision without talking to you. Share Phase 1 documents to demonstrate preparedness, then use Phase 2 as a reason for follow-up conversations. There is a principle of escalating commitment in negotiations that applies here: each interaction where the investor invests time (reviewing documents, asking questions, scheduling calls) makes them more likely to move forward. If you hand over everything on day one, you lose that advantage.

How to Prioritize Your Data Room

You don’t need everything day one. Here’s the timing framework:

Before you start fundraising, Phase 1 should be complete and clean. Reconcile financials that don’t balance, make sure the cap table is accurate, and have your pitch materials polished. For instance, a company raising a seed round should have a clean cap table, 12 months of monthly financials, and a current deck in one folder before the first investor meeting.

Before or during the term sheet process, Phase 2 should be organized and ready to share within 24-48 hours. Most investors won’t ask for corporate documents, employment agreements, or IP assignments until they’ve decided the business is worth pursuing. But when they do ask, respond quickly and completely, because each fast reply builds confidence while each “let me get back to you” erodes it.

If they ask: Phase 3 is deal-specific. Prepare it if you have time, but don’t let it delay the start of your raise.

Should You Even Build a Data Room?

There are two legitimate schools of thought here, and they contradict each other.

Mark Suster, Managing Partner at Upfront Ventures and a founder who sold two companies to Salesforce before becoming a VC, has argued that you should never have a data room ready. His reasoning: a pre-built data room removes urgency from the process and gives investors reasons to say no before they’ve developed conviction about your story. If you control the flow of information, you build the relationship first, get them excited, and provide documents as they request them. Each request becomes a touchpoint, and each response shows responsiveness and competence.

There’s real wisdom here, especially for hot rounds where multiple investors are competing, and the deal is moving fast.

But here’s the counter-argument, and the one I see play out more often: if you don’t have your documents organized before due diligence starts, you will look unorganized and unprofessional. Never give an investor an easy reason to ding you in the fundraising process. Assembling a data room under pressure exposes problems you didn’t know you had, and any one of them can stall a deal for weeks.

Charlie O’Donnell, a VC at Brooklyn Bridge Ventures, has talked extensively about how broken cap tables kill deals. His point: cap table issues that surface during diligence are almost never intentional fraud. These problems stem from founders who acted quickly, delayed hiring legal counsel, and established verbal agreements that were not adequately recorded.

My recommendation: build Phase 1 before you start conversations, have Phase 2 ready to assemble quickly, but control how and when you share documents rather than dumping everything into a folder on day one.

The Mistakes I See Most Often

Starting too late. This is by far the most common mistake: founders begin building the data room after the first investor meeting, which means they’re already behind by the time diligence starts. Build Phase 1 at least a month before you start having conversations.

Disorganized files. Investors review dozens of deals simultaneously. A data room filled with poorly named files scattered across random folders signals that the business is managed similarly. Use clear folder structure and logical file naming (date-first: “2026-03-25-Income-Statement-Monthly.xlsx”). Follow the folder setup described above and keep your master folder current.

Cap table errors. Cap table problems kill more deals than poor financial performance. Common issues include missing IP assignments, option grants that exceed the pool, and SAFE conversions that haven’t been modeled. Before you fundraise, get a cap table management tool (Carta, Pulley, or Cake Equity) and have a lawyer review the whole table.

Financial statements that don’t match the model. If historical financials show $50K in monthly revenue and projections assume $500K in month 12, you need a clear explanation of what changes. Investors will cross-reference your actuals with your projections, and if the two don’t connect through a plausible growth story, credibility drops fast.

Missing IP assignments. If a contractor or co-founder built core technology and there’s no signed IP assignment agreement, you have a ticking time bomb. Have your lawyer prepare standard IP assignment agreements and get them signed before due diligence starts.

Over-building the data room. Don’t spend weeks creating a 200-document data room before your first meeting. Get Phase 1 clean, have Phase 2 ready to assemble quickly, and focus your energy on building relationships and running the process. A data room that is 80% complete and available when the investor asks is worth more than one that is 100% complete but delayed the start of your raise by a month.

How to Use the Data Room Strategically

The best founders don’t dump documents in a folder. They treat the data room as a tool for managing the fundraising process, and the way they release information shapes how investors perceive the company.

Control the flow. Give investors Phase 1 when they enter diligence, then release Phase 2 as they go deeper. You maintain control of the information flow without withholding anything, and each document release becomes a reason to have another conversation. This approach works particularly well when you’re managing multiple investors on different timelines, because you can tailor the depth of what each investor sees to where they are in their process.

Track engagement. If you’ve upgraded to DocSend or Ansarada, you can see who’s viewing which documents and for how long. An investor who’s spent 45 minutes in your financial model is more serious than one who glanced at the deck for 30 seconds. Use that distinction to prioritize your time during the raise.

Update proactively. If metrics improve during the raise (and they should, because the rest of your team is still building), update the data room and tell investors. An update like “we closed our biggest customer” or “March revenue was 30% above plan” is often what moves a round from cold to hot.

The Bottom Line

The data room is not a bureaucratic exercise. It reflects how well you run the business, and investors read organizational quality as a proxy for operational quality. Clean documents and fast responses to diligence requests communicate competence. Messy documents, missing agreements, and slow responses communicate the opposite.

Build Phase 1 before you fundraise, have Phase 2 ready to deploy within 48 hours, and use the data room as a tool for managing the process rather than a box to check.

Further Reading

- Mark Suster: Why You Should Never Have a Data Room - the contrarian case, worth reading even if you disagree

- Carta: Due Diligence Guide - detailed walkthrough from the investor’s perspective

- Y Combinator: A Guide to Seed Fundraising - covers data room expectations within the broader fundraising process

If organizing corporate documents, cleaning up the cap table, and preparing financial statements for investor scrutiny feels overwhelming, ask for help. Prepare your company’s information thoroughly before investors review it to make your fundraising easier.

For a step-by-step fundraising process, see How to Raise Money for a Startup. For the full landscape of capital options, see How to Find Investors for a Small Business.