Should You Raise Venture Capital?

Venture capital is designed for a specific type of company. Here's how to know if that's yours, what you're signing up for, and what happens if you get it wrong.

Should You Raise Venture Capital?

The Short Answer

Sure, but only if you know what you’re getting into.

Venture capital is, by definition, not for most companies and not for most startups.

That is not a criticism.

Venture funds have a structural organization, investors (limited partners) have specific expectations, and the math of fund returns operates in a certain way.

The question is not whether VC is good or bad.

The question is whether VC is right for your company, given what you want to build, how fast you can grow, and what you’re willing to give up.

The Scale of Venture Capital

Some context on what you’re entering when you raise VC:

The global venture capital industry manages over $1.25 trillion in assets, with $314 billion deployed into startups in 2024 alone. The top 12 firms captured over 50% of capital raised in the first half of 2025. This is a concentrated, institutional market with clear rules about what it funds and why.

The median seed round in 2024 was $3 million. The average Series A was $18.7 million. By the time a company goes public, it has typically raised $100-500 million across multiple rounds over 7-12 years. That capital comes with expectations at every stage.

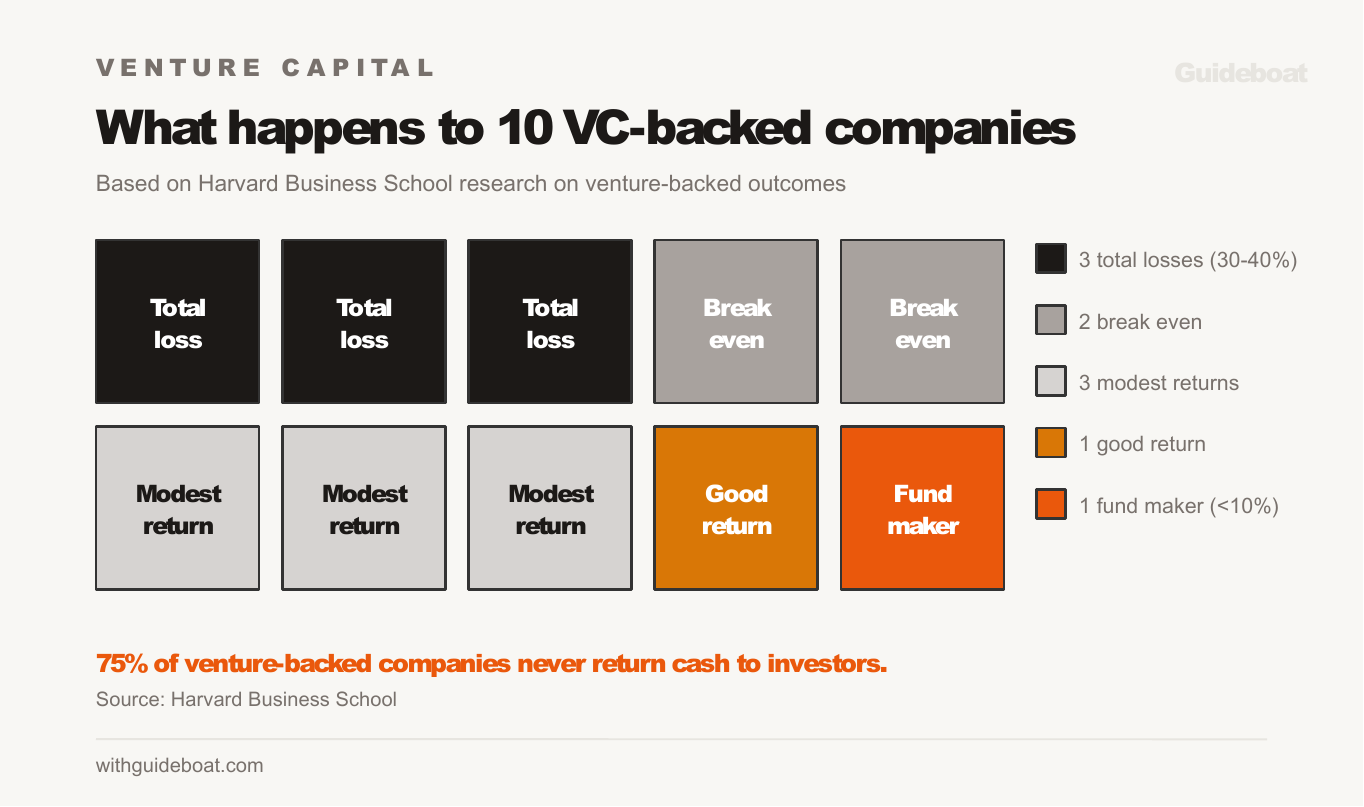

And the outcomes are brutal. Harvard Business School research found that 75% of venture-backed companies never return cash to investors. In 30-40% of cases, investors lose their entire investment. The companies that generate fund returns are a small minority of the portfolio.

That is the business model.

The Gates

When I work with founders, I don’t start with “Should you raise VC?” I start with “What do you really want? What do you really hope for?” The answers usually reveal the type of investor that best fits the company. But there are a few objective gates worth walking through first.

Gate 1: Is there a real billion-dollar market?

Venture funds need large outcomes to make their math work. A $200M fund that owns 15% of a company needs that company to be worth at least $1.3 billion to return the fund on one deal. Most funds expect that only 1-2 companies out of every 10 investments will produce that kind of return. Venture capitalists expect the rest to fail, return modest amounts, or break even.

If your addressable market is $50 million, you are not building a venture-scale company. That is not a problem. It means venture capital is not the right tool for funding your growth. There are other tools.

If your addressable market is $1-10 billion and you have a credible path to capturing a meaningful share of it, you’re in the range where venture investors will pay attention.

Gate 2: Can you scale exponentially?

Can the business go from $1M to $5M to $15M to $55M in annual revenue over a 5-7-year period? That trajectory (roughly 3x growth year over year, declining to 2x as the base gets larger) is the pre-AI benchmark for venture-backed revenue growth. The top 1% of AI companies grow revenue even faster. If the business grows linearly (20-30% per year, which is excellent growth for most companies), it will not generate the returns a venture fund needs.

Software companies can often scale this way because marginal costs are low. Hardware, manufacturing, CPG, and services businesses rarely can without massive capital expenditure, because each unit of growth requires proportional investment in production, inventory, or labor.

Gate 3: Do you need it to build the company you want?

Some companies have enormous capital requirements before they can generate revenue. A global autonomous robotics company needs tens of millions in R&D before it has a product to sell. A semiconductor company needs even more. For these companies, venture capital (or government grants) may be the only viable path because the upfront investment is too large for revenue or debt to fund.

Other companies don’t need outside capital at all. They can grow on revenue. The choice to raise VC is a choice about speed, not survival. That’s a valid reason to raise, but it’s important to be honest about whether you’re raising because you need the capital or because you want the validation and network that come with it.

Gate 4: Even in smaller markets, the growth math has to work

Not all VCs manage $1 billion funds. Some manage $50-100 million and invest in vertical software companies, niche B2B products, or regional businesses with strong competitive positions. These investors may be comfortable with a $200-500 million outcome. But the growth ramp and return potential still need to work. A company that plateaus at $5 million in revenue and grows 10% a year is not a fit for any venture fund, regardless of size.

What You’re Really Signing Up For

If your company passes the gates and you decide to raise VC, understand what you’re entering. This is not just a financial transaction. It is an existential choice.

Your existence depends on their capital and their future capital. Once you take venture money and build your company around a growth plan that assumes future fundraising, you depend on continuing to raise. If you cannot raise the next round, you will have to restructure the business radically or shut it down. There is very little middle ground.

If the company does not grow, investors will not put in more capital. Venture funds operate on portfolio theory. They invest in 20-30 companies, expecting that most will fail and a few will generate the returns that make the fund profitable. When a company is not growing, the fund’s rational response is to stop investing and allocate capital to the companies that are working. This is not personal. It is their fiduciary obligation to their own investors.

You may be able to generate free cash flow, but you’ll have to fight for it. If the business reaches a point where it could be profitable, but the board wants you to reinvest everything in growth, you have a governance conflict. The board may be right (growth is the priority) or wrong (the market doesn’t support that growth rate), but either way, you will be arguing for a strategy that serves the business against a board that serves the fund’s return model.

Even moderate success can be a bad outcome. If your company grows to $10M in revenue, is profitable, and has a strong team, that sounds like a success. But if your investors put in $15M at a $50M valuation, a $30M acquisition that would make you wealthy is a terrible deal for them. They will block it. You may be stuck running a company you’d rather sell because the terms of the investment require a larger outcome.

If the company goes to zero, the personal consequences vary. Some founders who build a real company that ultimately fails can credibly go back to investors as someone who has operated at scale. But you need a non-zero outcome (an acqui-hire, a modest sale, something that shows the company had real value) to maintain investor trust. A company that simply runs out of money with nothing to show for it is a harder story to tell.

The Dangerous Middle

The worst position is raising some money from investors who expect venture-scale outcomes when the business is naturally a lifestyle business. A small angel round or a few SAFEs from investors who need a 10x return, applied to a business that grows linearly and will never IPO.

Now you have minority shareholders with expectations the business can’t meet. The business cannot return the money. The business doesn’t have enough cashflow to buy out the investors, and in most circumstances a dividend payment will never return their initial capital. The bottom line is: you can’t decide to be a lifestyle business because you have contractual obligations to people with different goals.

Andrew Gazdecki, who built BusinessApps to $10M in annual revenue without raising venture capital, then built Acquire.com (the leading marketplace for startup acquisitions), has seen this pattern repeatedly. Many of the companies listed for sale on Acquire are profitable, growing businesses whose founders raised venture capital and now need to find an exit that their investors will accept.

The Alternatives

Venture capital is one source of funding, but it is not the only source.

Bootstrap with revenue. Grow at the pace your cash flow supports. Keep full control. Take as much money out of the business as you want. If you want to work 30 hours a week and make $500K a year, nobody will tell you that’s not ambitious enough.

Revenue-based financing. Borrow against your revenue and repay as a percentage of monthly income. No equity given up, no board seats, no exit pressure. Lighter Capital, Pipe, and Capchase all offer this. This makes sense in certain industries, and does not solve the 0 to 1 problem.

Angel-only rounds. Angel investors (especially those in your industry) provide capital without institutional pressure. Angels are often more patient and more aligned with moderate outcomes.

Non-dilutive capital. SBIR grants, SBA loans, and state programs provide capital without any equity impact.

Indie and patient capital funds. TinySeed and Calm Fund invest in profitable software companies and expect reasonable returns, not 100x.

How to Decide?

When I work with founders on this question, I ask them to answer honestly:

- What does success look like for you personally in 10 years?

- What size does this business need to be to achieve that?

- Does the market reward the fastest player disproportionately, or can multiple companies win?

- Can you fund the growth with revenue, or do you need outside capital to compete?

- Are you comfortable with investors having governance rights over major decisions?

- What is your personal financial runway if things take longer than expected?

If the answers point toward venture, go raise. Do it with open eyes and negotiate terms that protect your ability to operate. If the answers are mixed, don’t raise until you have more clarity. You can always raise money later. You can never un-raise it.

The Bottom Line

Venture capital is a powerful tool for a specific type of company: one with a large addressable market, the ability to scale exponentially, and a founder who wants to build something enormous and will accept the constraints and risks that come with institutional capital.

For everyone else, and that is most companies, there are better paths.

The most expensive mistake in startup fundraising isn’t raising at a bad valuation or picking the wrong investors. It’s raising money for a business that didn’t need it, or raising from investors whose expectations don’t match the business you’re building.

Further Reading

- NVCA 2025 Yearbook - industry data on VC deployment and fund performance

- Harvard Business School: The Venture Capital Secret - research on venture-backed company outcomes

- Acquire.com - a marketplace where you can see what happens when VC-backed companies need exits

Understanding what type of capital fits your business is one of the first conversations we have in a fractional CFO engagement. The decision about whether to raise venture capital shapes every financial decision that follows. How to Find Investors for a Small Business maps the full capital landscape beyond VC, and SAFE vs. Convertible Note vs. Priced Round covers the instruments you’ll encounter regardless of which path you choose.